![]()

By Dominik Krupke, TU Braunschweig

Many combinatorially difficult optimization problems can, despite their proven theoretical hardness, be solved reasonably well in practice. The most successful approach is to use Mixed Integer Linear Programming (MIP) to model the problem and then use a solver to find a solution. The most successful solvers for MIPs are Gurobi and CPLEX, which are both commercial and expensive (though, free for academics). There are also some open source solvers, but they are often not as powerful as the commercial ones. However, even when investing in such a solver, the underlying techniques (Branch and Bound & Cut on Linear Relaxations) struggle with some optimization problems, especially if the problem contains a lot of logical constraints that a solution has to satisfy. In this case, the Constraint Programming (CP) approach may be more successful. For Constraint Programming, there are many open source solvers, but they usually do not scale as well as MIP-solvers and are worse in optimizing objective functions. While MIP-solvers are frequently able to optimize problems with hundreds of thousands of variables and constraints, the classical CP-solvers often struggle with problems with more than a few thousand variables and constraints. However, the relatively new CP-SAT of Google's OR-Tools suite shows to overcome many of the weaknesses and provides a viable alternative to MIP-solvers, being competitive for many problems and sometimes even superior.

This unofficial primer shall help you use and understand this powerful tool, especially if you are coming from the Mixed Integer Linear Programming -community, as it may prove useful in cases where Branch and Bound performs poorly.

If you are relatively new to combinatorial optimization, I suggest you to read the relatively short book In Pursuit of the Traveling Salesman by Bill Cook first. It tells you a lot about the history and techniques to deal with combinatorial optimization problems, on the example of the famous Traveling Salesman Problem. The Traveling Salesman Problem seems to be intractable already for small instances, but it is actually possible to solve instances with thousands of cities in practice. It is a very light read and you can skip the more technical parts if you want to. As an alternative, you can also read this free chapter, coauthored by the same author and watch this very amusing YouTube Video (1hour). If you are short on time, at least watch the video, it is really worth it. While CP-SAT follows a slightly different approach than the one described in the book/chapter/video, it is still important to see why it is possible to do the seemingly impossible and solve such problems in practice, despite their theoretical hardness. Additionally, you will have learned the concept of Mathematical Programming, and know that the term "Programming" has nothing to do with programming in the sense of writing code (otherwise, additionally read the just given reference). The course Discrete Optimization on Coursera with Pascal Van Hentenryck and Carleton Coffrin is also highly recommendable and gives you an intense crash course on nearly all important topics in applied combinatorial optimization. After that (or if you are already familiar with combinatorial optimization), the following content awaits you in this primer:

Content:

- Installation: Quick installation guide.

- Example: A short example, showing the usage of CP-SAT.

- Modelling: An overview of variables, objectives, and constraints. The constraints make the most important part.

- Parameters: How to specify CP-SATs behavior, if needed. Timelimits, hints, assumptions, parallelization, ...

- Coding Patterns: Basic design patterns for creating maintainable algorithms.

- How does it work?: After we know what we can do with CP-SAT, we look into how CP-SAT will do all these things.

- Alternatives: An overview of the different optimization techniques and tools available. Putting CP-SAT into context.

- Benchmarking your Model: How to benchmark your model and how to interpret the results.

- Large Neighborhood Search: The use of CP-SAT to create more powerful heuristics.

Target audience: People (especially my students at TU Braunschweig) with some background in integer programming /linear optimization, who would like to know an actual viable alternative to Branch and Cut. However, I try to make it understandable for anyone interested in combinatorial optimization.

About the Main Author: Dr. Dominik Krupke is a postdoctoral researcher with the Algorithms Group at TU Braunschweig. He specializes in practical solutions to NP-hard problems. Initially focused on theoretical computer science, he now applies his expertise to solve what was once deemed impossible. This primer, first developed as course material for his students, has been extended in his spare time to cater to a wider audience.

Found a mistake? Please open an issue or a pull request. You can also just write me a quick mail to

krupked@gmail.com.

Want to Contribute? If you are interested in contributing, please open an issue or email me with a brief description of your proposal. We can then discuss the details. I welcome all assistance and am open to expanding the content. Contributors to any section or similar input will be recognized as coauthors.

Want to use/share this content? This tutorial can be freely used under CC-BY 4.0. Smaller parts can even be copied without any acknowledgement for non-commercial, educational purposes.

Why are there so many platypuses in the text? I enjoy incorporating elements in my texts that add a light-hearted touch. The choice of the platypus is intentional: much like CP-SAT integrates diverse elements from various domains, the platypus combines traits from different animals. It is a unique mammal that lays eggs, possesses a beak, and is venomous. The platypus also symbolizes Australia, home to the development of a key technique in CP-SAT - Lazy Clause Generation (LCG). Also, I like platypuses, and hope to see a real one someday.

We are using Python 3 in this primer and assume that you have a working Python 3 installation as well as the basic knowledge to use it. There are also interfaces for other languages, but Python 3 is, in my opinion, the most convenient one, as the mathematical expressions in Python are very close to the mathematical notation (allowing you to spot mathematical errors much faster). Only for huge models, you may need to use a compiled language such as C++ due to performance issues. For smaller models, you will not notice any performance difference.

The installation of CP-SAT, which is part of the OR-Tools package, is very easy and can be done via Python's package manager pip.

pip3 install -U ortoolsThis command will also update an existing installation of OR-Tools. As this tool is in active development, it is recommended to update it frequently. We actually encountered wrong behavior, i.e., bugs, in earlier versions that then have been fixed by updates (this was on some more advanced features, do not worry about correctness with basic usage).

I personally like to use Jupyter Notebooks for experimenting with CP-SAT.

It is important to note that for CP-SAT usage, you do not need the capabilities of a supercomputer. A standard laptop is often sufficient for solving many problems. The primary requirements are CPU power and memory bandwidth, with a GPU being unnecessary.

In terms of CPU power, the key is balancing the number of cores with the performance of each individual core. CP-SAT leverages all available cores, implementing different strategies on each. Depending on the number of cores, CP-SAT will behave differently. However, the effectiveness of these strategies can vary, and it is usually not apparent which one will be most effective. A higher single-core performance means that your primary strategy will operate more swiftly. I recommend a minimum of 4 cores and 16GB of RAM.

While CP-SAT is quite efficient in terms of memory usage, the amount of available memory can still be a limiting factor in the size of problems you can tackle. When it came to setting up our lab for extensive benchmarking at TU Braunschweig, we faced a choice between desktop machines and more expensive workstations or servers. We chose desktop machines equipped with AMD Ryzen 9 7900 CPUs (Intel would be equally suitable) and 96GB of DDR5 RAM, managed using Slurm. This decision was driven by the fact that the performance gains from higher-priced workstations or servers were relatively marginal compared to their significantly higher costs. When on the road, I am often still able to do stuff with my old Intel Macbook Pro from 2018 with an i7 and only 16GB of RAM, but large models will overwhelm it. My workstation at home with AMD Ryzen 7 5700X and 32GB of RAM on the other hand rarely has any problems with the models I am working on.

For further guidance, consider the hardware recommendations for the Gurobi solver, which are likely to be similar. Since we frequently use Gurobi in addition to CP-SAT, our hardware choices were also influenced by their recommendations.

Before we dive into any internals, let us take a quick look at a simple application of CP-SAT. This example is so simple that you could solve it by hand, but know that CP-SAT would (probably) be fine with you adding a thousand (maybe even ten- or hundred-thousand) variables and constraints more. The basic idea of using CP-SAT is, analogous to MIPs, to define an optimization problem in terms of variables, constraints, and objective function, and then let the solver find a solution for it. We call such a formulation that can be understood by the corresponding solver a model for the problem. For people not familiar with this declarative approach, you can compare it to SQL, where you also just state what data you want, not how to get it. However, it is not purely declarative, because it can still make a huge(!) difference how you model the problem and getting that right takes some experience and understanding of the internals. You can still get lucky for smaller problems (let us say a few hundred to thousands of variables) and obtain optimal solutions without having an idea of what is going on. The solvers can handle more and more 'bad' problem models effectively with every year.

Definition: A model in mathematical programming refers to a mathematical description of a problem, consisting of variables, constraints, and optionally an objective function that can be understood by the corresponding solver class. Modelling refers to transforming a problem (instance) into the corresponding framework, e.g., by making all constraints linear as required for Mixed Integer Linear Programming. Be aware that the SAT-community uses the term model to refer to a (feasible) variable assignment, i.e., solution of a SAT-formula. If you struggle with this terminology, maybe you want to read this short guide on Math Programming Modelling Basics.

Our first problem has no deeper meaning, except of showing the basic workflow of

creating the variables (x and y), adding the constraint

from ortools.sat.python import cp_model

model = cp_model.CpModel()

# Variables

x = model.NewIntVar(0, 100, "x") # you always need to specify an upper bound.

y = model.NewIntVar(0, 100, "y")

# there are also no continuous variables: You have to decide for a resolution and then work on integers.

# Constraints

model.Add(x + y <= 30)

# Objective

model.Maximize(30 * x + 50 * y)

# Solve

solver = cp_model.CpSolver() # Contrary to Gurobi, model and solver are separated.

status = solver.Solve(model)

assert (

status == cp_model.OPTIMAL

) # The status tells us if we were able to compute a solution.

print(f"x={solver.Value(x)}, y={solver.Value(y)}")

print("=====Stats:======")

print(solver.SolutionInfo())

print(solver.ResponseStats())x=0, y=30

=====Stats:======

default_lp

CpSolverResponse summary:

status: OPTIMAL

objective: 1500

best_bound: 1500

booleans: 1

conflicts: 0

branches: 1

propagations: 0

integer_propagations: 2

restarts: 1

lp_iterations: 0

walltime: 0.00289923

usertime: 0.00289951

deterministic_time: 8e-08

gap_integral: 5.11888e-07

Pretty easy, right? For solving a generic problem, not just one specific

instance, you would of course create a dictionary or list of variables and use

something like model.Add(sum(vars)<=n), because you do not want to create the

model by hand for larger instances.

The output you get may differ from the one above, because CP-SAT actually uses a set of different strategies in parallel, and just returns the best one (which can differ slightly between multiple runs due to additional randomness). This is called a portfolio strategy and is a common technique in combinatorial optimization, if you cannot predict which strategy will perform best.

In a later section, we will explore how to review and interpret the CP-SAT solver's log. Analyzing the log is vital, especially when the solver's performance is suboptimal. An expert can often pinpoint the cause of any issues within seconds by examining the log, which is key to optimizing solver efficiency.

The mathematical model of the code above would usually be written by experts something like this:

The s.t. stands for subject to, sometimes also read as such that.

One aspect of using CP-SAT solver that often poses challenges for learners is

understanding operator overloading in Python and the distinction between the two

types of variables involved. In this context, x and y serve as mathematical

variables. That is, they are placeholders that will only be assigned specific

values during the solving phase. To illustrate this more clearly, let us explore

an example within the Python shell:

>>> model = cp_model.CpModel()

>>> x = model.NewIntVar(0, 100, "x")

>>> x

x(0..100)

>>> type(x)

<class 'ortools.sat.python.cp_model.IntVar'>

>>> x + 1

sum(x(0..100), 1)

>>> x + 1 <= 1

<ortools.sat.python.cp_model.BoundedLinearExpression object at 0x7d8d5a765df0>In this example, x is not a conventional number but a placeholder defined to

potentially assume any value between 0 and 100. When 1 is added to x, the

result is a new placeholder representing the sum of x and 1. Similarly,

comparing this sum to 1 produces another placeholder, which encapsulates the

comparison of the sum with 1. These placeholders do not hold concrete values at

this stage but are essential for defining constraints within the model.

Attempting operations like if x + 1 <= 1: print("True") will trigger a

NotImplementedError, as the condition x+1<=1 cannot be evaluated directly.

Although this approach to defining models might initially seem perplexing, it facilitates a closer alignment with mathematical notation, which in turn can make it easier to identify and correct errors in the modeling process.

If you are not yet satisfied, this folder contains many Jupyter Notebooks with examples from the developers.

Ok. Now that you have seen a minimal model, let us next look on what options we have to model a problem. Note that an experienced optimizer may be able to model most problems with just the elements shown above, but showing your intentions may help CP-SAT optimize your problem better. Contrary to Mixed Integer Programming, you also do not need to fine-tune any Big-Ms (a reason to model higher-level constraints, such as conditional constraints that are only enforced if some variable is set to true, in MIPs yourself, because the computer is not very good at that).

![]()

CP-SAT provides us with much more modelling options than the classical

MIP-solver. Instead of just the classical linear constraints (<=, ==, >=), we

have various advanced constraints such as AllDifferent or

AddMultiplicationEquality. This spares you the burden of modelling the logic

only with linear constraints, but also makes the interface more extensive.

Additionally, you have to be aware that not all constraints are equally

efficient. The most efficient constraints are linear or boolean constraints.

Constraints such as AddMultiplicationEquality can be significantly(!!!) more

expensive.

Tip

If you are coming from the MIP-world, you should not overgeneralize your experience to CP-SAT as the underlying techniques are different. It does not rely on the linear relaxation as much as MIP-solvers do. Thus, you can often use modelling techniques that are not efficient in MIP-solvers, but perform reasonably well in CP-SAT. For example, I had a model that required multiple absolute values and performed significantly better in CP-SAT than in Gurobi (despite a manual implementation with relatively tight big-M values).

This primer does not have the space to teach about building good models. In the following, we will primarily look onto a selection of useful constraints. If you want to learn how to build models, you could take a look into the book Model Building in Mathematical Programming by H. Paul Williams which covers much more than you probably need, including some actual applications. This book is of course not for CP-SAT, but the general techniques and ideas carry over. However, it can also suffice to simply look on some other models and try some things out. If you are completely new to this area, you may want to check out modelling for the MIP-solver Gurobi in this video course. Remember that many things are similar to CP-SAT, but not everything (as already mentioned, CP-SAT is especially interesting for the cases where a MIP-solver fails).

The following part does not cover all constraints. You can get a complete

overview by looking into the

official documentation.

Simply go to CpModel and check out the AddXXX and NewXXX methods.

Resources on mathematical modelling (not CP-SAT specific):

- Math Programming Modeling Basics by Gurobi: Get the absolute basics.

- Modeling with Gurobi Python: A video course on modelling with Gurobi. The concepts carry over to CP-SAT.

- Model Building in Mathematical Programming by H. Paul Williams: A complete book on mathematical modelling.

Warning

CP-SAT 9.9 recently changed its API to be more consistent with the commonly

used Python style. Instead of NewIntVar, you can now also use new_int_var.

This primer still uses the old style, but will be updated in the future. I

observed cases where certain methods were not available in one or the other

style, so you may need to switch between them for some versions.

Elements:

- Variables

- Objectives

- Linear Constraints

- Logical Constraints (Propositional Logic)

- Conditional Constraints (Channeling, Reification)

- AllDifferent

- Absolute Values and Max/Min

- Multiplication, Division, and Modulo

- Circuit/Tour-Constraints

- Interval/Packing/Scheduling Constraints

- Piecewise Linear Constraints

There are two important types of variables in CP-SAT: Booleans and Integers (which are actually converted to Booleans, but more on this later). There are also, e.g., interval variables, but they are not as important and can be modelled easily with integer variables. For the integer variables, you have to specify a lower and an upper bound.

# integer variable z with bounds -100 <= z <= 100

z = model.NewIntVar(-100, 100, "z")

# boolean variable b

b = model.NewBoolVar("b")

# implicitly available negation of b:

not_b = b.Not() # will be 1 if b is 0 and 0 if b is 1Tip

Having tight bounds on the integer variables can make a huge impact on the performance. It may be useful to run some optimization heuristics beforehand to get some bounds. Reducing it by a few percent can already pay off for some problems.

There are no continuous/floating point variables (or even constants) in CP-SAT: If you need floating point numbers, you have to approximate them with integers by some resolution. For example, you could simply multiply all values by 100 for a step size of 0.01. A value of 2.35 would then be represented by 235. This could probably be implemented in CP-SAT directly, but doing it explicitly is not difficult, and it has numerical implications that you should be aware of.

The lack of continuous variables may sound like a serious limitation, especially if you have a background in linear optimization (where continuous variables are the "easy part"), but as long as they are not a huge part of your problem, you can often work around it. I had problems with many continuous variables on which I had to apply absolute values and conditional linear constraints, and CP-SAT performed much better than Gurobi, which is known to be very good at continuous variables. In this case, CP-SAT struggled less with the continuous variables (Gurobi's strength), than Gurobi with the logical constraints (CP-SAT's strength). In a further analysis, I noted an only logarithmic increase of the runtime with the resolution. However, there are also problems for which a higher resolution can drastically increase the runtime. The packing problem, which is discussed further below, has the following runtime for different resolutions: 1x: 0.02s, 10x: 0.7s, 100x: 7.6s, 1000x: 75s, 10_000x: >15min. The solution was always the same, just scaled, and there was no objective, i.e., only a feasible solution had to be found. Note that this is just an example, not a representative benchmark. See ./examples/add_no_overlap_2d_scaling.ipynb for the code. If you have a problem with a lot of continuous variables, such as network flow problems, you are probably better served with a MIP-solver.

In my experience, boolean variables are by far the most important variables in many combinatorial optimization problems. Many problems, such as the famous Traveling Salesman Problem, only consist of boolean variables. Implementing a solver specialized on boolean variables by using a SAT-solver as a base, such as CP-SAT, thus, is quite sensible. The resolution of coefficients (in combination with boolean variables) is less critical than for variables.

You might question the need for naming variables in your model. While it is true that CP-SAT would not need named variables to work (as it could just give them automatically generated names), assigning names is incredibly useful for debugging purposes. Solver APIs often create an internal representation of your model, which is subsequently used by the solver. There are instances where you might need to examine this internal model, such as when debugging issues like infeasibility. In such scenarios, having named variables can significantly enhance the clarity of the internal representation, making your debugging process much more manageable.

When dealing with integer variables that you know will only need to take certain values, or when you wish to limit their possible values, domain variables can become interesting. Unlike regular integer variables, domain variables are tailored to represent a specific set of values. This approach can enhance efficiency when the domain - the range of sensible values - is small. However, it may not be the best choice for larger domains.

CP-SAT works by converting all integer variables into boolean variables (warning: simplification). For each potential value, it creates two boolean variables: one indicating whether the integer variable is equal to this value, and another indicating whether it is less than or equal to it. This is called an order encoding. At first glance, this might suggest that using domain variables is always preferable, as it appears to reduce the number of boolean variables needed.

However, CP-SAT employs a lazy creation strategy for these boolean variables. This means it only generates them as needed, based on the solver's decision-making process. Therefore, an integer variable with a wide range - say, from 0 to 100 - will not immediately result in 200 boolean variables. It might lead to the creation of only a few, depending on the solver's requirements.

Limiting the domain of a variable can have drawbacks. Firstly, defining a domain explicitly can be computationally costly and increase the model size drastically as it now need to contain not just a lower and upper bound for a variable but an explicit list of numbers (model size is often a limiting factor). Secondly, by narrowing down the solution space, you might inadvertently make it more challenging for the solver to find a viable solution. First, try to let CP-SAT handle the domain of your variables itself and only intervene if you have a good reason to do so.

If you choose to utilize domain variables for their benefits in specific scenarios, here is how to define them:

from ortools.sat.python import cp_model

# Define a domain with selected values

domain = cp_model.Domain.FromValues([2, 5, 8, 10, 20, 50, 90])

# cam also be done via intervals

domain_2 = cp_model.Domain.FromIntervals([(8, 12), (14, 20)])

# Create a domain variable within this defined domain

x = model.NewIntVarFromDomain(domain, "x")This example illustrates the process of creating a domain variable x that can

only take on the values specified in domain. This method is particularly

useful when you are working with variables that only have a meaningful range of

possible values within your problem's context.

Not every problem actually has an objective, sometimes you only need to find a feasible solution. CP-SAT is pretty good at doing that (MIP-solvers are often not). However, CP-SAT can also optimize pretty well (older constraint programming solver cannot, at least in my experience). You can minimize or maximize a linear expression (use auxiliary variables and constraints to model more complicated expressions).

You can specify the objective function by calling model.Minimize or

model.Maximize with a linear expression.

model.Maximize(30 * x + 50 * y)Let us look on how to model more complicated expressions, using boolean variables and generators.

x_vars = [model.NewBoolVar(f"x{i}") for i in range(10)]

model.Minimize(

sum(i * x_vars[i] if i % 2 == 0 else i * x_vars[i].Not() for i in range(10))

)This objective evaluates to

To implement a lexicographic optimization, you can do multiple rounds and always fix the previous objective as constraint.

model.Maximize(30 * x + 50 * y)

# Lexicographic

solver.Solve(model)

model.Add(30 * x + 50 * y == int(solver.ObjectiveValue())) # fix previous objective

model.Minimize(z) # optimize for second objective

solver.Solve(model)To implement non-linear objectives, you can use auxiliary variables and constraints. For example, you can create a variable that is the absolute value of another variable and then use this variable in the objective.

abs_x = model.NewIntVar(0, 100, "|x|")

model.AddAbsEquality(target=abs_x, expr=x)

model.Minimize(abs_x)The available constraints are discussed next.

These are the classical constraints also used in linear optimization. Remember that you are still not allowed to use floating point numbers within it. Same as for linear optimization: You are not allowed to multiply a variable with anything else than a constant and also not to apply any further mathematical operations.

model.Add(10 * x + 15 * y <= 10)

model.Add(x + z == 2 * y)

# This one actually is not linear but still works.

model.Add(x + y != z)

# For <, > you can simply use <= and -1 because we are working on integers.

model.Add(x <= z - 1) # x < zNote that != can be expected slower than the other (<=, >=, ==)

constraints, because it is not a linear constraint. If you have a set of

mutually != variables, it is better to use AllDifferent (see below) than to

use the explicit != constraints.

Warning

If you use intersecting linear constraints, you may get problems because the intersection point needs to be integral. There is no such thing as a feasibility tolerance as in Mixed Integer Programming-solvers, where small deviations are allowed. The feasibility tolerance in MIP-solvers allows, e.g., 0.763445 == 0.763439 to still be considered equal to counter numerical issues of floating point arithmetic. In CP-SAT, you have to make sure that values can match exactly.

You can actually model logical constraints also as linear constraints, but it may be advantageous to show your intent:

b1 = model.NewBoolVar("b1")

b2 = model.NewBoolVar("b2")

b3 = model.NewBoolVar("b3")

model.AddBoolOr(b1, b2, b3) # b1 or b2 or b3 (at least one)

model.AddBoolAnd(b1, b2.Not(), b3.Not()) # b1 and not b2 and not b3 (all)

model.AddBoolAnd(b1, ~b2, ~b3) # Alternative notation for `Not()`

model.AddBoolXOr(b1, b2, b3) # b1 xor b2 xor b3

model.AddImplication(b1, b2) # b1 -> b2In this context you could also mention AddAtLeastOne, AddAtMostOne, and

AddExactlyOne, but these can also be modelled as linear constraints.

Linear constraints (Add), BoolOr, and BoolAnd support being activated by a condition. This is not only a very helpful constraint for many applications, but it is also a constraint that is highly inefficient to model with linear optimization (Big M Method). My current experience shows that CP-SAT can work much more efficiently with this kind of constraint. Note that you only can use a boolean variable and not directly add an expression, i.e., maybe you need to create an auxiliary variable.

model.Add(x + z == 2 * y).OnlyEnforceIf(b1)

model.Add(x + z == 10).OnlyEnforceIf([b2, b3.Not()]) # only enforce if b2 AND NOT b3

# Restrict domain of linear expression on condition

x_b = model.NewBoolVar("x_b")

x_i = model.NEwIntVar(0, 100, "x_i")

domain = model.Domain.FromValues([0, 10, 20, 30, 40, 50])

model.AddLinearExpressionInDomain(x_i, domain).OnlyEnforceIf(x_b)A constraint that is often seen in Constraint Programming, but I myself was always able to deal without it. Still, you may find it important. It forces all (integer) variables to have a different value.

AllDifferent is actually the only constraint that may use a domain based

propagator (if it is not a permutation)

[source]

model.AddAllDifferent(x, y, z)

# You can also add a constant to the variables.

vars = [model.NewIntVar(0, 10) for i in range(10)]

model.AddAllDifferent(x + i for i, x in enumerate(vars))The N-queens example of the official tutorial makes use of this constraint.

There is a big caveat with this constraint: CP-SAT now has a preprocessing step

that automatically tries to infer large AllDifferent constraints from sets of

mutual != constraints. This inference equals the NP-hard Edge Clique Cover

problem, thus, is not a trivial task. If you add an AllDifferent constraint

yourself, CP-SAT will assume that you already took care of this inference and

will skip this step. Thus, adding a single AllDifferent constraint can make

your model significantly slower, if you also use != constraints. If you do not

use != constraints, you can safely use AllDifferent without any performance

penalty. You may also want to use != instead of AllDifferent if you apply it

to overlapping sets of variables without proper optimization, because then

CP-SAT will do the inference for you.

In

./examples/add_all_different.ipynb

you can find a quick experiment based on the graph coloring problem. In the

graph coloring problem, the colors of two adjacent vertices have to be

different. This can be easily modelled by != or AllDifferent constraints on

every edge. Using !=, we can solve the example graph in around 5 seconds. If

we use AllDifferent, it takes more than 5 minutes. If we manually disable the

AllDifferent inference, it also takes more than 5 minutes. Same if we add just

a single AllDifferent constraint. Thus, if you use AllDifferent do it

properly on large sets, or use != constraints and let CP-SAT infer the

AllDifferent constraints for you.

Maybe CP-SAT will allow you to use AllDifferent without any performance

penalty in the future, but for now, you have to be aware of this. See also

the optimization parameter documentation.

Two often occurring and important operators are absolute values as well as minimum and maximum values. You cannot use operators directly in the constraints, but you can use them via an auxiliary variable and a dedicated constraint. These constraints are more efficient than comparable constraints in classical MIP-solvers, but you should still not overuse them.

# abs_xz == |x+z|

abs_xz = model.NewIntVar(0, 200, "|x+z|") # ub = ub(x)+ub(z)

model.AddAbsEquality(target=abs_xz, expr=x + z)

# max_xyz = max(x,y,z)

max_xyz = model.NewIntVar(0, 100, "max(x,y, z)")

model.AddMaxEquality(max_xyz, [x, y, z])

# min_xyz = min(x,y,z)

min_xyz = model.NewIntVar(-100, 100, " min(x,y, z)")

model.AddMinEquality(min_xyz, [x, y, z])Also note that surprisingly often, you can replace these constraints with more efficient linear constraints. Here is one example for the max equality:

x = model.NewIntVar(0, 100, "x")

y = model.NewIntVar(0, 100, "y")

z = model.NewIntVar(0, 100, "z")

# enforce that max_xyz has to be at least the maximum of x, y, z

max_xyz = model.NewIntVar(0, 100, "max_xyz")

model.Add(max_xyz >= x)

model.Add(max_xyz >= y)

model.Add(max_xyz >= z)

# as we minimized max_xyz, it has to be the maximum of x, y, z

model.Minimize(max_xyz)This example illustrates that enforcing the exact maximum value is not always

necessary; a lower bound suffices. By minimizing the variable, the model itself

enforces tightness. Although this approach requires more constraints, it

utilizes constraints that are significantly more efficient than the

AddMaxEquality constraint, typically resulting in faster solving times.

Additional techniques exist for managing minimum and absolute values, as well as for complex scenarios where the objective function does not directly enforce equality. Experienced optimizers can often swiftly identify opportunities to replace standard constraints with more efficient alternatives. However, employing these advanced techniques should follow the acquisition of sufficient experience or the use of a verified base model for comparison. From my consulting experience with optimization models, I have found that resolving issues from improperly applied optimizations frequently requires more time than applying these techniques initially to a model that uses the less efficient constraints.

A big nono in linear optimization (the most successful optimization area) are multiplication of variables (because this would no longer be linear, right...). Often we can linearize the model by some tricks and tools like Gurobi are also able to do some non-linear optimization ( in the end, it is most often translated to a less efficient linear model again). CP-SAT can also work with multiplication and modulo of variables, again as constraint not as operation. So far, I have not made good experience with these constraints, i.e., the models end up being slow to solve, and would recommend to only use them if you really need them and cannot find a way around them.

xyz = model.NewIntVar(-100 * 100 * 100, 100**3, "x*y*z")

model.AddMultiplicationEquality(xyz, [x, y, z]) # xyz = x*y*z

model.AddModuloEquality(x, y, 3) # x = y % 3

model.AddDivisionEquality(x, y, z) # x = y // zYou can very often approximate these constraints with significantly more efficient linear constraints, even if it may require some additional variables or reification. Doing a piecewise linear approximation can be an option even for more complex functions, though they too are not necessarily efficient.

Certain quadratic constraints, e.g., second-order cones, can be efficiently handled by interior point methods, as utilized by the Gurobi solver. However, CP-SAT currently lacks this capability and needs to do significantly more work to handle these constraints. Long story short, if you can avoid these constraints, you should do so, even if you have to give up on modelling the exact function you had in mind.

Warning

The documentation indicates that multiplication of more than two variables is supported, but I got an error when trying it out. I have not investigated this further, as I would expect it to be painfully slow anyway.

The Traveling Salesman Problem (TSP) or Hamiltonicity Problem are important and difficult problems that occur as subproblem in many contexts. For solving the classical TSP, you should use the extremely powerful solver Concorde. There is also a separate part in OR-Tools dedicated to routing. If it is just a subproblem, you can add a simple constraint by encoding the allowed edges as triples of start vertex index, target vertex index, and literal/variable. Note that this is using directed edges/arcs. By adding a triple (v,v,var), you can allow CP-SAT to skip the vertex v.

Tip

If the tour-problem is the fundamental part of your problem, you may be better served with using a Mixed Integer Programming solver. Do not expect to solve tours much larger than 250 vertices with CP-SAT.

from ortools.sat.python import cp_model

# Weighted, directed graph as instance

# (source, destination) -> cost

dgraph = {

(0, 1): 13,

(1, 0): 17,

(1, 2): 16,

(2, 1): 19,

(0, 2): 22,

(2, 0): 14,

(3, 0): 15,

(3, 1): 28,

(3, 2): 25,

(0, 3): 24,

(1, 3): 11,

(2, 3): 27,

}

model = cp_model.CpModel()

# Variables: Binary decision variables for the edges

edge_vars = {(u, v): model.NewBoolVar(f"e_{u}_{v}") for (u, v) in dgraph.keys()}

# Constraints: Add Circuit constraint

# We need to tell CP-SAT which variable corresponds to which edge.

# This is done by passing a list of tuples (u,v,var) to AddCircuit.

circuit = [

(u, v, var) for (u, v), var in edge_vars.items() # (source, destination, variable)

]

model.AddCircuit(circuit)

# Objective: minimize the total cost of edges

obj = sum(dgraph[(u, v)] * x for (u, v), x in edge_vars.items())

model.Minimize(obj)

# Solve

solver = cp_model.CpSolver()

status = solver.Solve(model)

assert status in (cp_model.OPTIMAL, cp_model.FEASIBLE)

tour = [(u, v) for (u, v), x in edge_vars.items() if solver.Value(x)]

print("Tour:", tour)Tour: [(0, 1), (2, 0), (3, 2), (1, 3)]

You can use this constraint very flexibly for many tour problems. We added three examples:

- ./examples/add_circuit.py: The example above, slightly extended. Find out how large you can make the graph.

- ./examples/add_circuit_budget.py: Find the largest tour with a given budget. This will be a bit more difficult to solve.

-

./examples/add_circuit_multi_tour.py:

Allow

$k$ tours, which in sum need to be minimal and cover all vertices.

The most powerful TSP-solver concorde uses a linear programming based

approach, but with a lot of additional techniques to improve the performance.

The book In Pursuit of the Traveling Salesman by William Cook may have already

given you some insights. For more details, you can also read the more advanced

book The Traveling Salesman Problem: A Computational Study by Applegate,

Bixby, Chvatál, and Cook. If you need to solve some variant, MIP-solvers (which

could be called a generalization of that approach) are known to perform well

using the

Dantzig-Fulkerson-Johnson Formulation.

This model is theoretically exponential, but using lazy constraints (which are

added when needed), it can be solved efficiently in practice. The

Miller-Tucker-Zemlin formulation

allows a small formulation size, but is bad in practice with MIP-solvers due to

its weak linear relaxations. Because CP-SAT does not allow lazy constraints, the

Danzig-Fulkerson-Johnson formulation would require many iterations and a lot of

wasted resources. As CP-SAT does not suffer as much from weak linear relaxations

(replacing Big-M by logic constraints, such as OnlyEnforceIf), the

Miller-Tucker-Zemlin formulation may be an option in some cases, though a simple

experiment (see below) shows a similar performance as the iterative approach.

When using AddCircuit, CP-SAT will actually use the LP-technique for the

linear relaxation (so using this constraint may really help, as otherwise CP-SAT

will not know that your manual constraints are actually a tour with a nice

linear relaxation), and probably has the lazy constraints implemented

internally. Using the AddCircuit constraint is thus highly recommendable for

any circle or path constraints.

In ./examples/add_circuit_comparison.ipynb, we compare the performance of some models for the TSP, to estimate the performance of CP-SAT for the TSP.

- AddCircuit can solve the Euclidean TSP up to a size of around 110 vertices in 10 seconds to optimality.

- MTZ (Miller-Tucker-Zemlin) can solve the eculidean TSP up to a size of around 50 vertices in 10 seconds to optimality.

- Dantzig-Fulkerson-Johnson via iterative solving can solve the eculidean TSP up to a size of around 50 vertices in 10 seconds to optimality.

- Dantzig-Fulkerson-Johnson via lazy constraints in Gurobi can solve the eculidean TSP up to a size of around 225 vertices in 10 seconds to optimality.

This tells you to use a MIP-solver for problems dominated by the tour

constraint, and if you have to use CP-SAT, you should definitely use the

AddCircuit constraint.

Warning

These are all naive implementations, and the benchmark is not very rigorous. These values are only meant to give you a rough idea of the performance. Additionally, this benchmark was regarding proving optimality. The performance in just optimizing a tour could be different. The numbers could also look different for differently generated instances. You can find a more detailed benchmark in the later section on proper evaluation.

Here is the performance of AddCircuit for the TSP on some instances (rounded

eucl. distance) from the TSPLIB with a time limit of 90 seconds.

| Instance | # nodes | runtime | lower bound | objective | opt. gap |

|---|---|---|---|---|---|

| att48 | 48 | 0.47 | 33522 | 33522 | 0 |

| eil51 | 51 | 0.69 | 426 | 426 | 0 |

| st70 | 70 | 0.8 | 675 | 675 | 0 |

| eil76 | 76 | 2.49 | 538 | 538 | 0 |

| pr76 | 76 | 54.36 | 108159 | 108159 | 0 |

| kroD100 | 100 | 9.72 | 21294 | 21294 | 0 |

| kroC100 | 100 | 5.57 | 20749 | 20749 | 0 |

| kroB100 | 100 | 6.2 | 22141 | 22141 | 0 |

| kroE100 | 100 | 9.06 | 22049 | 22068 | 0 |

| kroA100 | 100 | 8.41 | 21282 | 21282 | 0 |

| eil101 | 101 | 2.24 | 629 | 629 | 0 |

| lin105 | 105 | 1.37 | 14379 | 14379 | 0 |

| pr107 | 107 | 1.2 | 44303 | 44303 | 0 |

| pr124 | 124 | 33.8 | 59009 | 59030 | 0 |

| pr136 | 136 | 35.98 | 96767 | 96861 | 0 |

| pr144 | 144 | 21.27 | 58534 | 58571 | 0 |

| kroB150 | 150 | 58.44 | 26130 | 26130 | 0 |

| kroA150 | 150 | 90.94 | 26498 | 26977 | 2% |

| pr152 | 152 | 15.28 | 73682 | 73682 | 0 |

| kroA200 | 200 | 90.99 | 29209 | 29459 | 1% |

| kroB200 | 200 | 31.69 | 29437 | 29437 | 0 |

| pr226 | 226 | 74.61 | 80369 | 80369 | 0 |

| gil262 | 262 | 91.58 | 2365 | 2416 | 2% |

| pr264 | 264 | 92.03 | 49121 | 49512 | 1% |

| pr299 | 299 | 92.18 | 47709 | 49217 | 3% |

| linhp318 | 318 | 92.45 | 41915 | 52032 | 19% |

| lin318 | 318 | 92.43 | 41915 | 52025 | 19% |

| pr439 | 439 | 94.22 | 105610 | 163452 | 35% |

You can even go completely bonkers and work with arrays in your model. The

element at a variable index can be accessed via an AddElement constraint.

The second constraint is actually more of a stable matching in array form. For

two arrays of variables

# ai = [x,y,z][i] assign ai the value of the i-th entry.

ai = model.NewIntVar(-100, 100, "a[i]")

i = model.NewIntVar(0, 2, "i")

model.AddElement(index=i, variables=[x, y, z], target=ai)

model.AddInverse([x, y, z], [z, y, x])A special case of variables are the interval variables, that allow to model intervals, i.e., a span of some length with a start and an end. There are fixed length intervals, flexible length intervals, and optional intervals to model various use cases. These intervals become interesting in combination with the no-overlap constraints for 1D and 2D. We can use this for geometric packing problems, scheduling problems, and many other problems, where we have to prevent overlaps between intervals. These variables are special because they are actually not a variable, but a container that bounds separately defined start, length, and end variables.

from ortools.sat.python import cp_model

start_var = model.NewIntVar(0, 100, "start")

length_var = model.NewIntVar(10, 20, "length")

end_var = model.NewIntVar(0, 100, "end")

is_present_var = model.NewBoolVar("is_present")

# creating an interval of fixed length

fixed_interval = model.NewFixedSizeIntervalVar(

start=start_var, size=10, end=end_var, name="fixed_interval"

)

# creating an interval whose length can be influenced by a variable (more expensive)

flexible_interval = model.NewIntervalVar(

start=start_var, size=length_var, end=end_var, name="flexible_interval"

)

# creating an interval that can be present or not

optional_fixed_interval = model.NewOptionalFixedSizeIntervalVar(

start=start_var,

size=10,

end=end_var,

is_present=is_present_var,

name="optional_fixed_interval",

)

# creating an interval that can be present or not and whose length can be influenced by a variable (most expensive)

optional_interval = model.NewOptionalIntervalVar(

start=start_var,

size=length_var,

end=end_var,

is_present=is_present_var,

name="optional_interval",

)There are now the two no-overlap constraints for 1D and 2D that can be used to prevent overlaps between intervals. The 1D no-overlap constraint is used to prevent overlaps between intervals on a single dimension, e.g., time. The 2D no-overlap constraint is used to prevent overlaps between intervals on two dimensions, e.g., time and resources or for packing rectangles.

# 1D no-overlap constraint

model.AddNoOverlap([__INTERVAL_VARS__])

# 2D no-overlap constraint. The two lists need to have the same length.

model.AddNoOverlap2D(

[__INTERVAL_VARS_FIRST_DIMENSION__], [__INTERVAL_VARS_SECOND_DIMENSION__]

)Let us take a quick look on how we can use this to check if we can pack a set of rectangles into a container without overlaps. This can be an interesting problem in logistics, where we have to pack boxes into a container, or in cutting stock problems, where we have to cut pieces from a larger piece of material.

class RectanglePackingWithoutRotationsModel:

def __init__(self, instance: Instance) -> None:

self.instance = instance

self.model = cp_model.CpModel()

# We have to create the variable for the bottom left corner of the boxes.

# We directly limit their range, such that the boxes are inside the container

self.x_vars = [

self.model.NewIntVar(

0, instance.container.width - box.width, name=f"x1_{i}"

)

for i, box in enumerate(instance.rectangles)

]

self.y_vars = [

self.model.NewIntVar(

0, instance.container.height - box.height, name=f"y1_{i}"

)

for i, box in enumerate(instance.rectangles)

]

# Interval variables are actually more like constraint containers, that are then passed to the no overlap constraint

# Note that we could also make size and end variables, but we do not need them here

x_interval_vars = [

self.model.NewFixedSizeIntervalVar(

start=self.x_vars[i], # the x value of the bottom left corner

size=box.width, # the width of the rectangle

name=f"x_interval_{i}",

)

for i, box in enumerate(instance.rectangles)

]

y_interval_vars = [

self.model.NewFixedSizeIntervalVar(

start=self.y_vars[i], # the y value of the bottom left corner

size=box.height, # the height of the rectangle

name=f"y_interval_{i}",

)

for i, box in enumerate(instance.rectangles)

]

# Enforce that no two rectangles overlap

self.model.AddNoOverlap2D(x_interval_vars, y_interval_vars)

def _extract_solution(self, solver: cp_model.CpSolver) -> Optional[Solution]:

if self.status not in (cp_model.OPTIMAL, cp_model.FEASIBLE):

return None

placements = []

for i, box in enumerate(self.instance.rectangles):

x = solver.Value(self.x_vars[i])

y = solver.Value(self.y_vars[i])

placements.append(Placement(x=x, y=y))

return Solution(placements=placements)

def solve(self, time_limit: float = 900.0):

solver = cp_model.CpSolver()

solver.parameters.log_search_progress = True

solver.parameters.max_time_in_seconds = time_limit

self.status = solver.Solve(self.model)

self.solution = self._extract_solution(solver)

self.upper_bound = solver.BestObjectiveBound()

self.objective_value = solver.ObjectiveValue()

return self.status

def is_infeasible(self):

return self.status == cp_model.INFEASIBLE

def is_feasible(self):

return self.status in (cp_model.OPTIMAL, cp_model.FEASIBLE)The optional intervals with flexible length allow us to even model rotations and instead of just checking if a feasible packing exists, finding the largest possible packing. The code may look a bit more complex, but considering the complexity of the problem, it is still quite simple.

class RectangleKnapsackWithRotationsModel:

def __init__(self, instance: Instance) -> None:

self.instance = instance

self.model = cp_model.CpModel()

# Create coordinates for the placement. We need variables for the begin and end of each rectangle.

# This will also ensure that the rectangles are placed inside the container.

self.bottom_left_x_vars = [

self.model.NewIntVar(0, instance.container.width, name=f"x1_{i}")

for i, box in enumerate(instance.rectangles)

]

self.bottom_left_y_vars = [

self.model.NewIntVar(0, instance.container.height, name=f"y1_{i}")

for i, box in enumerate(instance.rectangles)

]

self.upper_right_x_vars = [

self.model.NewIntVar(0, instance.container.width, name=f"x2_{i}")

for i, box in enumerate(instance.rectangles)

]

self.upper_right_y_vars = [

self.model.NewIntVar(0, instance.container.height, name=f"y2_{i}")

for i, box in enumerate(instance.rectangles)

]

# These variables indicate if a rectangle is rotated or not

self.rotated_vars = [

self.model.NewBoolVar(f"rotated_{i}")

for i in range(len(instance.rectangles))

]

# Depending on if a rectangle is rotated or not, we have to adjust the width and height variables

self.width_vars = [

self.model.NewIntVar(0, max(box.width, box.height), name=f"width_{i}")

for i, box in enumerate(instance.rectangles)

]

self.height_vars = [

self.model.NewIntVar(0, max(box.width, box.height), name=f"height_{i}")

for i, box in enumerate(instance.rectangles)

]

# Here we enforce that the width and height variables are correctly set

for i, box in enumerate(instance.rectangles):

if box.width > box.height:

diff = box.width - box.height

self.model.Add(

self.width_vars[i] == box.width - self.rotated_vars[i] * diff

)

self.model.Add(

self.height_vars[i] == box.height + self.rotated_vars[i] * diff

)

else:

diff = box.height - box.width

self.model.Add(

self.width_vars[i] == box.width + self.rotated_vars[i] * diff

)

self.model.Add(

self.height_vars[i] == box.height - self.rotated_vars[i] * diff

)

# And finally, a variable indicating if a rectangle is packed or not

self.packed_vars = [

self.model.NewBoolVar(f"packed_{i}")

for i in range(len(instance.rectangles))

]

# Interval variables are actually more like constraint containers, that are then passed to the no overlap constraint

# Note that we could also make size and end variables, but we do not need them here

self.x_interval_vars = [

self.model.NewOptionalIntervalVar(

start=self.bottom_left_x_vars[i],

size=self.width_vars[i],

is_present=self.packed_vars[i],

end=self.upper_right_x_vars[i],

name=f"x_interval_{i}",

)

for i, box in enumerate(instance.rectangles)

]

self.y_interval_vars = [

self.model.NewOptionalIntervalVar(

start=self.bottom_left_y_vars[i],

size=self.height_vars[i],

is_present=self.packed_vars[i],

end=self.upper_right_y_vars[i],

name=f"y_interval_{i}",

)

for i, box in enumerate(instance.rectangles)

]

# Enforce that no two rectangles overlap

self.model.AddNoOverlap2D(self.x_interval_vars, self.y_interval_vars)

# maximize the number of packed rectangles

self.model.Maximize(

sum(

box.value * self.packed_vars[i]

for i, box in enumerate(instance.rectangles)

)

)

def _extract_solution(self, solver: cp_model.CpSolver) -> Optional[Solution]:

if self.status not in (cp_model.OPTIMAL, cp_model.FEASIBLE):

return None

placements = []

for i, box in enumerate(self.instance.rectangles):

if solver.Value(self.packed_vars[i]):

placements.append(

Placement(

x=solver.Value(self.bottom_left_x_vars[i]),

y=solver.Value(self.bottom_left_y_vars[i]),

rotated=bool(solver.Value(self.rotated_vars[i])),

)

)

else:

placements.append(None)

return Solution(placements=placements)

def solve(self, time_limit: float = 900.0, opt_tol: float = 0.01):

solver = cp_model.CpSolver()

solver.parameters.log_search_progress = True

solver.parameters.max_time_in_seconds = time_limit

solver.parameters.relative_gap_limit = opt_tol

self.status = solver.Solve(self.model)

self.solution = self._extract_solution(solver)

self.upper_bound = solver.BestObjectiveBound()

self.objective_value = solver.ObjectiveValue()

return self.status |

|---|

| This dense packing was found by CP-SAT in less than 0.3s, which is quite impressive and seems to be more efficient than a naive Gurobi implementation. |

You can find the full code here:

| Problem Variant | Code |

|---|---|

| Deciding feasibility of packing rectangles without rotations | ./evaluations/packing/solver/packing_wo_rotations.py |

| Finding the largest possible packing of rectangles without rotations | ./evaluations/packing/solver/knapsack_wo_rotations.py |

| Deciding feasibility of packing rectangles with rotations | ./evaluations/packing/solver/packing_with_rotations.py |

| Finding the largest possible packing of rectangles with rotations | ./evaluations/packing/solver/knapsack_with_rotations.py |

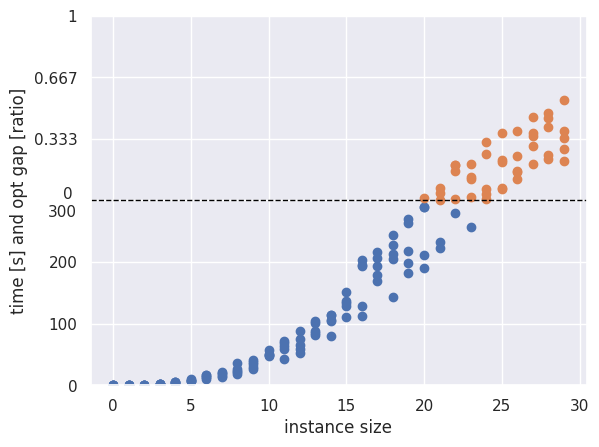

CP-SAT is good at finding a feasible packing, but incapable of proofing infeasibility in most cases. When using the knapsack variant, it can still pack most of the rectangles even for the larger instances.

|

|---|

| The number of solved instances for the packing problem (90s time limit). Rotations make things slightly more difficult. None of the used instances were proofed infeasible. |

|

| However, CP-SAT is able to pack nearly all rectangles even for the largest instances. |

In earlier versions of CP-SAT, the performance of no-overlap constraints was greatly influenced by the resolution. This impact has evolved, yet it remains somewhat inconsistent. In a notebook example, I explored how resolution affects the execution time of the no-overlap constraint in versions 9.3 and 9.8 of CP-SAT. For version 9.3, there is a noticeable increase in execution time as the resolution grows. Conversely, in version 9.8, execution time actually reduces when the resolution is higher, a finding supported by repeated tests. This unexpected behavior suggests that the performance of CP-SAT regarding no-overlap constraints has not stabilized and may continue to vary in upcoming versions.

| Resolution | Runtime (CP-SAT 9.3) | Runtime (CP-SAT 9.8) |

|---|---|---|

| 1x | 0.02s | 0.03s |

| 10x | 0.7s | 0.02s |

| 100x | 7.6s | 1.1s |

| 1000x | 75s | 40.3s |

| 10_000x | >15min | 0.4s |

This notebook was used to create the table above.

However, while playing around with less documented features, I noticed that the performance for the older version can be improved drastically with the following parameters:

solver.parameters.use_energetic_reasoning_in_no_overlap_2d = True

solver.parameters.use_timetabling_in_no_overlap_2d = True

solver.parameters.use_pairwise_reasoning_in_no_overlap_2d = TrueWith the latest version of CP-SAT, I did not notice a significant difference in performance when using these parameters.

In practice, you often have cost functions that are not linear. For example, consider a production problem where you have three different items you produce. Each item has different components, you have to buy. The cost of the components will first decrease with the amount you buy, then at some point increase again as your supplier will be out of stock and you have to buy from a more expensive supplier. Additionally, you only have a certain amount of customers willing to pay a certain price for your product. If you want to sell more, you will have to lower the price, which will decrease your profit.

Let us assume such a function looks like

|

|---|

| We can model an arbitrary continuous function with a piecewise linear function. Here, we split the original function into a number of straight segments. The accuracy can be adapted to the requirements. The linear segments can then be expressed in CP-SAT. The fewer such segments, the easier it remains to model and solve. |

Using linear constraints (model.Add) and reification (.OnlyEnforceIf), we

can model such a piecewise linear function in CP-SAT. For this we simply use

boolean variables to decide for a segment, and then activate the corresponding

linear constraint via reification. However, this has two problems in CP-SAT, as

shown in the next figure.

|

|---|

| Even if the function f(x) now consists of linear segments, we cannot simply implement |

-

Problem A: Even if we can express a segment as a linear function, the result of the function may not be integral. In the example,

$f(5)$ would be$3.5$ and, thus, if we enforce$y=f(x)$ ,$x$ would be prohibited to be$5$ , which is not what we want. There are two options now. Either, we use a more complex piecewise linear approximation that ensures that the function will always yield integral solutions or we use inequalities instead. The first solution has the issue that this can require too many segments, making it far too expensive to optimize. The second solution will be a weaker constraint as now we can only enforce$y<=f(x)$ or$y>=f(x)$ , but not$y=f(x)$ . If you try to enforce it by$y<=f(x)$ and$y>=f(x)$ , you will end with the same infeasibility as before. However, often an inequality will be enough. If the problem is to prevent$y$ from becoming too large, you use$y<=f(x)$ , if the problem is to prevent$y$ from becoming too small, you use$y>=f(x)$ . If we want to represent the costs by$f(x)$ , we would use$y>=f(x)$ to minimize the costs. -

Problem B: The canonical representation of a linear function is

$y=ax+b$ . However, this will often require non-integral coefficients. Luckily, we can automatically scale them up to integral values by adding a scaling factor. The inequality$y=0.5x+0.5$ in the example can also be represented as$2y=x+1$ . I will spare you the math, but it just requires a simple trick with the least common multiple. Of course, the required scaling factor can become large, and at some point lead to overflows.

An implementation could now look as follows:

# We want to enforce y=f(x)

x = model.NewIntVar(0, 7, "x")

y = model.NewIntVar(0, 5, "y")

# use boolean variables to decide for a segment

segment_active = [model.NewBoolVar("segment_1"), model.NewBoolVar("segment_2")]

model.AddAtMostOne(segment_active) # enforce one segment to be active

# Segment 1

# if 0<=x<=3, then y >= 0.5*x + 0.5

model.Add(2 * y >= x + 1).OnlyEnforceIf(segment_active[0])

model.Add(x >= 0).OnlyEnforceIf(segment_active[0])

model.Add(x <= 3).OnlyEnforceIf(segment_active[0])

# Segment 2

model.Add(_SLIGHTLY_MORE_COMPLEX_INEQUALITY_).OnlyEnforceIf(segment_active[1])

model.Add(x >= 3).OnlyEnforceIf(segment_active[1])

model.Add(x <= 7).OnlyEnforceIf(segment_active[1])

model.Minimize(y)

# if we were to maximize y, we would have used <= instead of >=This can be quite tedious, but luckily, I wrote a small helper class that will do this automatically for you. You can find it in ./utils/piecewise_functions. Simply copy it into your code.

This code does some further optimizations:

- Considering every segment as a separate case can be quite expensive and inefficient. Thus, it can make a serious difference if you can combine multiple segments into a single case. This can be achieved by detecting convex ranges, as the constraints of convex areas do not interfere with each other.

- Adding the convex hull of the segments as a redundant constraint that does

not depend on any

OnlyEnforceIfcan in some cases help the solver to find better bounds.OnlyEnforceIf-constraints are often not very good for the linear relaxation, and having the convex hull as independent constraint can directly limit the solution space, without having to do any branching on the cases.

Let us use this code to solve an instance of the problem above.

We have two products that each require three components. The first product requires 3 of component 1, 5 of component 2, and 2 of component 3. The second product requires 2 of component 1, 1 of component 2, and 3 of component 3. We can buy up to 1500 of each component for the price given in the figure below. We can produce up to 300 of each product and sell them for the price given in the figure below.

|

|

|---|---|

| Costs for buying components necessary for production. | Selling price for the products. |

We want to maximize the profit, i.e., the selling price minus the costs for buying the components. We can model this as follows:

requirements_1 = (3, 5, 2)

requirements_2 = (2, 1, 3)

from ortools.sat.python import cp_model

model = cp_model.CpModel()

buy_1 = model.NewIntVar(0, 1_500, "buy_1")

buy_2 = model.NewIntVar(0, 1_500, "buy_2")

buy_3 = model.NewIntVar(0, 1_500, "buy_3")

produce_1 = model.NewIntVar(0, 300, "produce_1")

produce_2 = model.NewIntVar(0, 300, "produce_2")

model.Add(produce_1 * requirements_1[0] + produce_2 * requirements_2[0] <= buy_1)

model.Add(produce_1 * requirements_1[1] + produce_2 * requirements_2[1] <= buy_2)

model.Add(produce_1 * requirements_1[2] + produce_2 * requirements_2[2] <= buy_3)

# You can find this code it ./utils!

from piecewise_functions import PiecewiseLinearFunction, PiecewiseLinearConstraint

# Define the functions for the costs

costs_1 = [(0, 0), (1000, 400), (1500, 1300)]

costs_2 = [(0, 0), (300, 300), (700, 500), (1200, 600), (1500, 1100)]

costs_3 = [(0, 0), (200, 400), (500, 700), (1000, 900), (1500, 1500)]

# PiecewiseLinearFunction is a pydantic model and can be serialized easily!

f_costs_1 = PiecewiseLinearFunction(

xs=[x for x, y in costs_1], ys=[y for x, y in costs_1]

)

f_costs_2 = PiecewiseLinearFunction(

xs=[x for x, y in costs_2], ys=[y for x, y in costs_2]

)

f_costs_3 = PiecewiseLinearFunction(

xs=[x for x, y in costs_3], ys=[y for x, y in costs_3]

)

# Define the functions for the gain

gain_1 = [(0, 0), (100, 800), (200, 1600), (300, 2_000)]

gain_2 = [(0, 0), (80, 1_000), (150, 1_300), (200, 1_400), (300, 1_500)]

f_gain_1 = PiecewiseLinearFunction(xs=[x for x, y in gain_1], ys=[y for x, y in gain_1])

f_gain_2 = PiecewiseLinearFunction(xs=[x for x, y in gain_2], ys=[y for x, y in gain_2])

# Create y>=f(x) constraints for the costs

x_costs_1 = PiecewiseLinearConstraint(model, buy_1, f_costs_1, upper_bound=False)

x_costs_2 = PiecewiseLinearConstraint(model, buy_2, f_costs_2, upper_bound=False)

x_costs_3 = PiecewiseLinearConstraint(model, buy_3, f_costs_3, upper_bound=False)

# Create y<=f(x) constraints for the gain

x_gain_1 = PiecewiseLinearConstraint(model, produce_1, f_gain_1, upper_bound=True)

x_gain_2 = PiecewiseLinearConstraint(model, produce_2, f_gain_2, upper_bound=True)

# Maximize the gain minus the costs

model.Maximize(x_gain_1.y + x_gain_2.y - (x_costs_1.y + x_costs_2.y + x_costs_3.y))

solver = cp_model.CpSolver()

solver.parameters.log_search_progress = True

status = solver.Solve(model)

print(f"Buy {solver.Value(buy_1)} of component 1")

print(f"Buy {solver.Value(buy_2)} of component 2")

print(f"Buy {solver.Value(buy_3)} of component 3")

print(f"Produce {solver.Value(produce_1)} of product 1")

print(f"Produce {solver.Value(produce_2)} of product 2")

print(f"Overall gain: {solver.ObjectiveValue()}")This will give you the following output:

Buy 930 of component 1

Buy 1200 of component 2

Buy 870 of component 3

Produce 210 of product 1

Produce 150 of product 2

Overall gain: 1120.0

Unfortunately, these problems quickly get very complicated to model and solve. This is just a proof that, theoretically, you can model such problems in CP-SAT. Practically, you can lose a lot of time and sanity with this if you are not an expert.

CP-SAT has even more constraints, but I think I covered the most important ones. If you need more, you can check out the official documentation.

![]()

The CP-SAT solver has a lot of parameters to control its behavior. They are

implemented via

Protocol Buffer and can be

manipulated via the parameters-member. If you want to find out all options,

you can check the reasonably well documented proto-file in the

official repository.

I will give you the most important right below.

⚠️ Only a few of the parameters (e.g., timelimit) are beginner-friendly. Most other parameters (e.g., decision strategies) should not be touched as the defaults are well-chosen, and it is likely that you will interfere with some optimizations. If you need a better performance, try to improve your model of the optimization problem.

If we have a huge model, CP-SAT may not be able to solve it to optimality (if the constraints are not too difficult, there is a good chance we still get a good solution). Of course, we do not want CP-SAT to run endlessly for hours (years, decades,...) but simply abort after a fixed time and return us the best solution so far. If you are now asking yourself why you should use a tool that may run forever: There are simply no provably faster algorithms and considering the combinatorial complexity, it is incredible that it works so well. Those not familiar with the concepts of NP-hardness and combinatorial complexity, I recommend reading the book 'In Pursuit of the Traveling Salesman' by William Cook. Actually, I recommend this book to anyone into optimization: It is a beautiful and light weekend-read.

To set a time limit (in seconds), we can simply set the following value before we run the solver:

solver.parameters.max_time_in_seconds = 60 # 60s timelimitWe now of course have the problem, that maybe we will not have an optimal solution, or a solution at all, we can continue on. Thus, we need to check the status of the solver.

status = solver.Solve(model)

if status == cp_model.OPTIMAL or status == cp_model.FEASIBLE:

print("We have a solution.")

else:

print("Help?! No solution available! :( ")The following status codes are possible:

OPTIMAL: Perfect, we have an optimal solution.FEASIBLE: Good, we have at least a feasible solution (we may also have a bound available to check the quality viasolver.BestObjectiveBound()).INFEASIBLE: There is a proof that no solution can satisfy all our constraints.MODEL_INVALID: You used CP-SAT wrongly.UNKNOWN: No solution was found, but also no infeasibility proof. Thus, we actually know nothing. Maybe there is at least a bound available?

If you want to print the status, you can use solver.StatusName(status).

We can not only limit the runtime but also tell CP-SAT, we are satisfied with a

solution within a specific, provable quality range. For this, we can set the

parameters absolute_gap_limit and relative_gap_limit. The absolute limit

tells CP-SAT to stop as soon as the solution is at most a specific value apart

to the bound, the relative limit is relative to the bound. More specifically,

CP-SAT will stop as soon as the objective value(O) is within relative ratio

solver.parameters.relative_gap_limit = 0.05Now we may want to stop after we did not make progress for some time or whatever. In this case, we can make use of the solution callbacks.

For those familiar with Gurobi: Unfortunately, we can only abort the solution progress and not add lazy constraints or similar. For those not familiar with Gurobi or MIPs: With Mixed Integer Programming we can adapt the model during the solution process via callbacks which allows us to solve problems with many(!) constraints by only adding them lazily. This is currently the biggest shortcoming of CP-SAT for me. Sometimes you can still do dynamic model building with only little overhead feeding information of previous iterations into the model

For adding a solution callback, we have to inherit from a base class. The documentation of the base class and the available operations can be found in the documentation.

class MySolutionCallback(cp_model.CpSolverSolutionCallback):

def __init__(self, stuff):

cp_model.CpSolverSolutionCallback.__init__(self)

self.stuff = stuff # just to show that we can save some data in the callback.

def on_solution_callback(self):

obj = self.ObjectiveValue() # best solution value

bound = self.BestObjectiveBound() # best bound

print(f"The current value of x is {self.Value(x)}")

if abs(obj - bound) < 10:

self.StopSearch() # abort search for better solution

# ...

solver.Solve(model, MySolutionCallback(None))You can find an official example of using such callbacks .

Beside querying the objective value of the currently best solution, the solution

itself, and the best known bound, you can also find out about internals such as

NumBooleans(self), NumConflicts(self), NumBranches(self). What those

values mean will be discussed later.

With version 9.10, CP-SAT also supports bound callbacks. These are called when CP-SAT is able to improve the proven bound. As the solution callback is only called when a new solution is found, you may want to additionally use the bound callback when you want to abort the search as soon as the bound is good enough.

solver = cp_model.CpSolver()

def bound_callback(bound):

print(f"New bound: {bound}")

if bound > 100:

solver.StopSearch()

solver.best_bound_callback = bound_callbackYou can also try to directly hook into the log output of CP-SAT, which should be

called for new solutions, new bounds, and other important events. This can be

done by setting the log_callback parameter.

solver.log_callback = lambda msg: print("LOG:", msg) # (str)->NoneCP-SAT is a portfolio-solver that uses different techniques to solve the problem. There is some information exchange between the different workers, but it does not split the solution space into different parts, thus, it does not parallelize the branch-and-bound algorithm as MIP-solvers do. This can lead to some redundancy in the search, but running different techniques in parallel will also increase the chance of running the right technique. Predicting which technique will be the best for a specific problem is often hard, thus, this parallelization can be quite useful.

You can control the parallelization of CP-SAT by setting the number of search workers.

solver.parameters.num_search_workers = 8 # use 8 coresHere the solvers used by CP-SAT 9.9 on different parallelization levels for an optimization problem and no additional specifications (e.g., decision strategies). Note that some parameters/constraints/objectives can change the parallelization strategy Also check the official documentation.

solver.parameters.num_search_workers = 1: Single-threaded search with[default_lp].- 1 full problem subsolver: [default_lp]

solver.parameters.num_search_workers = 2: Additional use of heuristics to support thedefault_lpsearch.- 1 full problem subsolver: [default_lp]

- 13 incomplete subsolvers: [feasibility_pump, graph_arc_lns, graph_cst_lns, graph_dec_lns, graph_var_lns, packing_precedences_lns, packing_rectangles_lns, packing_slice_lns, rins/rens, rnd_cst_lns, rnd_var_lns, scheduling_precedences_lns, violation_ls]

- 3 helper subsolvers: [neighborhood_helper, synchronization_agent, update_gap_integral]

solver.parameters.num_search_workers = 3: Using a second full problem solver that does not try to linearize the model.- 2 full problem subsolvers: [default_lp, no_lp]

- 13 incomplete subsolvers: [feasibility_pump, graph_arc_lns, graph_cst_lns, graph_dec_lns, graph_var_lns, packing_precedences_lns, packing_rectangles_lns, packing_slice_lns, rins/rens, rnd_cst_lns, rnd_var_lns, scheduling_precedences_lns, violation_ls]

- 3 helper subsolvers: [neighborhood_helper, synchronization_agent, update_gap_integral]

solver.parameters.num_search_workers = 4: Additionally using a third full problem solver that tries to linearize the model as much as possible.- 3 full problem subsolvers: [default_lp, max_lp, no_lp]

- 13 incomplete subsolvers: [feasibility_pump, graph_arc_lns, graph_cst_lns, graph_dec_lns, graph_var_lns, packing_precedences_lns, packing_rectangles_lns, packing_slice_lns, rins/rens, rnd_cst_lns, rnd_var_lns, scheduling_precedences_lns, violation_ls]

- 3 helper subsolvers: [neighborhood_helper, synchronization_agent, update_gap_integral]

solver.parameters.num_search_workers = 5: Additionally using a first solution subsolver.- 3 full problem subsolvers: [default_lp, max_lp, no_lp]

- 1 first solution subsolver: [fj_short_default]

- 13 incomplete subsolvers: [feasibility_pump, graph_arc_lns, graph_cst_lns, graph_dec_lns, graph_var_lns, packing_precedences_lns, packing_rectangles_lns, packing_slice_lns, rins/rens, rnd_cst_lns, rnd_var_lns, scheduling_precedences_lns, violation_ls]

- 3 helper subsolvers: [neighborhood_helper, synchronization_agent, update_gap_integral]

solver.parameters.num_search_workers = 6: Using a fourth full problem solverquick_restartthat does more "probing".- 4 full problem subsolvers: [default_lp, max_lp, no_lp, quick_restart]

- 1 first solution subsolver: [fj_short_default]

- 13 incomplete subsolvers: [feasibility_pump, graph_arc_lns, graph_cst_lns, graph_dec_lns, graph_var_lns, packing_precedences_lns, packing_rectangles_lns, packing_slice_lns, rins/rens, rnd_cst_lns, rnd_var_lns, scheduling_precedences_lns, violation_ls]

- 3 helper subsolvers: [neighborhood_helper, synchronization_agent, update_gap_integral]

solver.parameters.num_search_workers = 7:- 5 full problem subsolvers: [default_lp, max_lp, no_lp, quick_restart, reduced_costs]

- 1 first solution subsolver: [fj_short_default]

- 13 incomplete subsolvers: [feasibility_pump, graph_arc_lns, graph_cst_lns, graph_dec_lns, graph_var_lns, packing_precedences_lns, packing_rectangles_lns, packing_slice_lns, rins/rens, rnd_cst_lns, rnd_var_lns, scheduling_precedences_lns, violation_ls]

- 3 helper subsolvers: [neighborhood_helper, synchronization_agent, update_gap_integral]

solver.parameters.num_search_workers = 8:- 6 full problem subsolvers: [default_lp, max_lp, no_lp, quick_restart, quick_restart_no_lp, reduced_costs]

- 1 first solution subsolver: [fj_short_default]

- 13 incomplete subsolvers: [feasibility_pump, graph_arc_lns, graph_cst_lns, graph_dec_lns, graph_var_lns, packing_precedences_lns, packing_rectangles_lns, packing_slice_lns, rins/rens, rnd_cst_lns, rnd_var_lns, scheduling_precedences_lns, violation_ls]

- 3 helper subsolvers: [neighborhood_helper, synchronization_agent, update_gap_integral]

solver.parameters.num_search_workers = 12:- 8 full problem subsolvers: [default_lp, lb_tree_search, max_lp, no_lp, pseudo_costs, quick_restart, quick_restart_no_lp, reduced_costs]

- 3 first solution subsolvers: [fj_long_default, fj_short_default, fs_random]

- 13 incomplete subsolvers: [feasibility_pump, graph_arc_lns, graph_cst_lns, graph_dec_lns, graph_var_lns, packing_precedences_lns, packing_rectangles_lns, packing_slice_lns, rins/rens, rnd_cst_lns, rnd_var_lns, scheduling_precedences_lns, violation_ls]

- 3 helper subsolvers: [neighborhood_helper, synchronization_agent, update_gap_integral]

solver.parameters.num_search_workers = 16:- 11 full problem subsolvers: [default_lp, lb_tree_search, max_lp, no_lp, objective_lb_search, objective_shaving_search_no_lp, probing, pseudo_costs, quick_restart, quick_restart_no_lp, reduced_costs]

- 4 first solution subsolvers: [fj_long_default, fj_short_default, fs_random, fs_random_quick_restart]